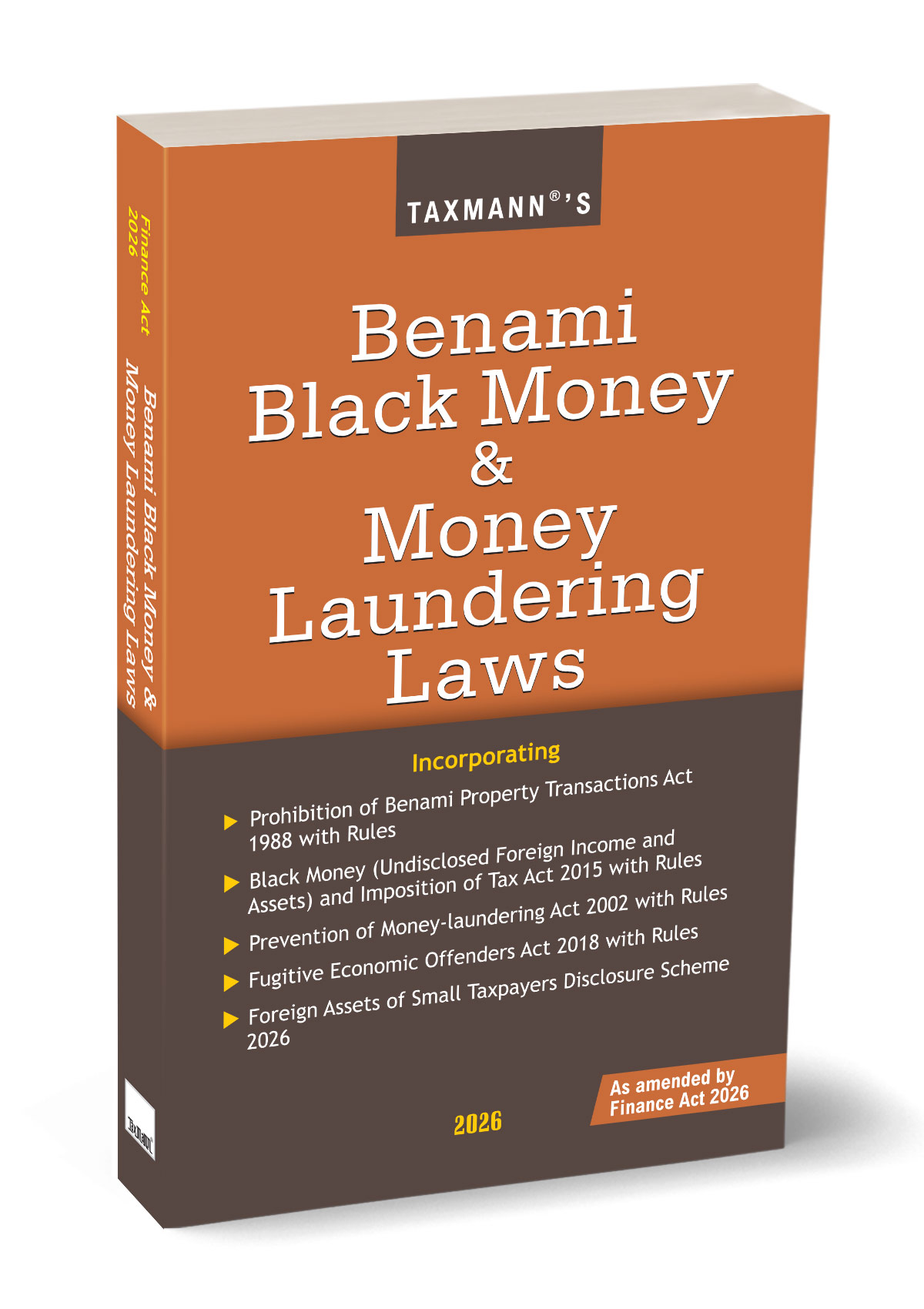

Description

India’s enforcement architecture against illicit wealth, concealed assets, and cross-border financial offences rests on a cluster of interlocking statutes—each with its own procedural framework, adjudicatory hierarchy, and penal consequence. Taxmann’s Benami Black Money & Money Laundering Laws is the authoritative single-volume reference that consolidates all five of these foundational laws in their current, fully amended form. The 2026 Edition has been updated to incorporate every amendment effected by the Finance Act 2026—including the newly enacted Foreign Assets of Small Taxpayers Disclosure Scheme 2026 (Sections 130–144 of the Finance Act 2026), which makes its debut in this Edition as a standalone Division.

The volume captures the complete and evolving text of the Prohibition of Benami Property Transactions Act 1988, the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act 2015, the Fugitive Economic Offenders Act 2018, and the Prevention of Money-Laundering Act 2002—each accompanied by their subsidiary rules, regulations, circulars, notifications, and, where applicable, the governing case law. With 588 pages and a scope that ranges from the foundational definitions of ‘benami transaction’ and ‘proceeds of crime’ to the procedural mechanics of attachment, adjudication, confiscation, and prosecution, this volume serves as the practitioner’s complete reference for India’s anti-black money statutory regime.

This title is designed for a wide but specialised readership:

Advocates and Litigators appearing before the Adjudicating Authority, Appellate Tribunal, Special Courts under PMLA and the Benami Act, and High Courts

Chartered Accountants, Company Secretaries, and Tax Professionals advising clients on compliance, disclosures, and enforcement risk under the Black Money Act and PMLA

Enforcement Directorate and Income Tax Officers engaged in investigation, attachment, and adjudication under these statutes

Corporate Counsel and Compliance Teams with exposure to AML obligations, KYC requirements, and reporting entity obligations under PMLA

Academicians and Researchers in tax law, financial crime, and public law

High-net-worth Individuals and NRIs with undisclosed foreign assets who may benefit from the 2026 Disclosure Scheme

Banks, NBFCs, and Other Reporting Entities subject to Aadhaar authentication mandates and maintenance-of-records obligations under PMLA

The Present Publication is the 2026 Edition and amended by the Finance Act 2026. This book is edited by Taxmann’s Editorial Board with the following coverage.

[Comprehensive Statutory Coverage] Five major statutes—together with their full complement of subsidiary rules, scheme regulations, and adjudicatory regulations—are consolidated in a single, coherently organised volume, eliminating the need to cross-reference multiple bare acts and gazette compilations

[Updated to Finance Act 2026] The Black Money Act 2015, the PMLA 2002, and the Benami Act 1988 are reproduced with all amendments incorporated up to and including the Finance Act 2026. Each provision carries precise amendment footnotes indicating the amending act, the date of effect, and the text of the superseded provision, enabling readers to trace the legislative history of every section

[Foreign Assets of Small Taxpayers Disclosure Scheme 2026] Division Five is new to the 2026 Edition. It reproduces, in full, Sections 130 to 144 of the Finance Act, 2026—the complete statutory text of the Disclosure Scheme providing a limited-window amnesty for small taxpayers with undisclosed foreign assets not exceeding ₹1 crore, with a structured tax-plus-penalty regime and immunity from prosecution

[Embedded Case Law] The Benami Transactions Act and Black Money Act divisions contain annotated case law under individual sections—drawn from Supreme Court and High Court decisions—providing immediate judicial context to each provision without the need to consult a separate digest

[Official Notifications and Circulars] Every division carries the relevant official gazette notifications, CBDT circulars, and ministerial instructions applicable to that statute, including PMLA notifications relating to Aadhaar authentication by reporting entities, appointment of Special Public Prosecutors across all States and Union Territories, and KYC record-keeping obligations for SEBI-registered intermediaries

[Complete Rules and Scheme Texts] All subsidiary rules, including the seven sets of Fugitive Economic Offenders Rules 2018 and the full suite of Prevention of Money-Laundering Rules 2005—are reproduced in their complete and current form, along with the Adjudicating Authority (Procedure) Regulations 2013

[Amendment Trail Transparency] Throughout the text, every substituted, inserted, or omitted provision is footnoted with the amending instrument and effective date, and, importantly, the prior text of the substituted or omitted provision is reproduced verbatim in the footnotes. This enables practitioners to establish the state of the law at any given point in the amendment history, which is especially significant in enforcement proceedings where the relevant provision depends on the date of the alleged transaction

[Benami Transactions Informants Reward Scheme 2018] This Division also includes the complete Reward Scheme, enabling reporting and compliance officers to advise on both enforcement risk and informant mechanics

The coverage of the book is as follows:

Division One | Prohibition of Benami Property Transactions Act 1988 with Rules — The foundational anti-benami statute, as comprehensively overhauled by the Benami Transactions (Prohibition) Amendment Act 2016 and further amended through the Finance Acts of 2019, 2020, 2021, 2023, 2024, and the Finance (No. 2) Acts of 2019 and 2024. Coverage includes:

Full statutory text of all 72 sections across eight Chapters, with omitted sections retained and their prior text reproduced in footnotes

Key definitional provisions, including the expanded four-limb definition of ‘benami transaction’ under Section 2(9) and its exceptions for HUF transactions, fiduciary arrangements, spousal/lineal transfers, and joint-ownership structures

Detailed procedural provisions on notice, provisional attachment (extended to four months by the Finance (No. 2) Act, 2024), adjudication, confiscation, and vesting

Appellate Tribunal constitution, qualification, procedure, and jurisdiction, including the restructured Adjudicating Authority mechanism following the Finance Act 2021’s merger of the Adjudicating Authority with the SAFEMA competent authority

Special Courts for criminal prosecution; offences and penalties, including Section 53 (rigorous imprisonment and fine for benami transactions) and Section 54 (penalty for false information)

Immunity from prosecution under Section 55A

Prohibition of Benami Property Transactions Rules 2016 (as amended)

Conditions of Service of Members of Adjudicating Authority Rules 2019

Benami Transactions Informants Reward Scheme 2018

Relevant notifications

Case law annotations are integrated under key sections, particularly Sections 2(9), 2(19), 24, 26, and 27, covering landmark Supreme Court and High Court decisions on the prospective application of the 2016 Amendment, jurisdictional validity of Initiating Officers, and e-gazette notification dates

Division Two | Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act 2015 with Rules — The primary statute targeting Indian residents’ undisclosed foreign income and assets, as amended by the Finance Act 2026. Coverage includes:

Complete statutory text with all Finance Act amendments incorporated

Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Rules 2015

Undisclosed Foreign Income and Assets Challan

CBDT Instructions Regarding Handling of Income-tax Cases and Black Money Cases

Extensive CBDT FAQs and circulars addressing: the scope of ‘undisclosed foreign asset,’ the interaction between DTAA information-sharing and disclosure eligibility, Schedule FA reporting obligations, the treatment of partially-explained assets, and the consequences of non-declaration in an era of Automatic Exchange of Information (AEOI) under FATCA and CRS

Division Three | Fugitive Economic Offenders Act 2018 with Rules — The statute enabling confiscation of the properties of persons who have left India to evade prosecution for scheduled offences. Coverage includes:

Full text of the Fugitive Economic Offenders Act 2018

Six sets of Rules 2018 governing: the form and manner of filing applications for declaration; attachment of property; issuance of provisional attachment orders; conduct of search and seizure; receipt and management of confiscated properties; and procedure for sending letters of request to contracting states

Relevant notifications

Division Four | Prevention of Money-Laundering Act 2002 with Rules — The most expansive Division in the volume, reflecting PMLA’s role as the cornerstone of India’s anti-money laundering framework. Coverage includes:

Full text of PMLA 2002 as amended up to date (all Chapters, Sections 2 through 75)

Thirteen sets of Rules and Regulations:

Manner of Forwarding Provisional Attachment Orders to the Adjudicating Authority Rules, 2005

Receipt and Management of Confiscated Properties Rules 2005

Maintenance of Records Rules 2005 (with KYC and CKYCRR amendments)

Forms, Search and Seizure or Freezing Rules 2005

Manner of Forwarding Arrest Order Rules 2005

Manner of Forwarding Order of Retention of Seized Property Rules 2005

Manner of Receiving Records Authenticated Outside India Rules 2005

Appeal Rules 2005

Adjudicating Authority (Procedure) Regulations 2013

Issuance of Provisional Attachment Order Rules 2013

Taking Possession of Attached or Frozen Properties Rules 2013

Restoration of Property Rules 2016

Extensive notifications covering:

Aadhaar authentication authorisation for reporting entities (banks, NBFCs, mutual funds, insurance companies, SEBI-registered intermediaries, fintech entities) under Section 11A, including notifications up to October 2025

Appointment of Special Public Prosecutors across all zones and States under Section 46, as updated through December 2024 and September 2025, including under the Bharatiya Nagarik Suraksha Sanhita 2023

Designation of the Director, Financial Intelligence Unit-India as Nodal Officer under Section 13 read with Section 79 of the IT Act 2000

SEBI-registered intermediary KYC upload and retrieval through KRA and CKYCRR

Division Five | Foreign Assets of Small Taxpayers Disclosure Scheme 2026 — A complete reproduction of Chapter IV of the Finance Act 2026 (Sections 130 to 144), constituting the Foreign Assets of Small Taxpayers Disclosure Scheme, 2026. Key provisions include:

Eligibility – Resident assessees (and non-residents/not-ordinarily-resident who were resident in the relevant previous year) with undisclosed foreign assets or income

Declaration Window – Open-ended from the date of commencement on notification, until the ‘last date’ as notified by the Central Government

Tax and Penalty Structure –

For undisclosed foreign assets/income not exceeding ₹1 crore in aggregate: 30% tax on asset value/income, plus 100% of such tax as penalty—totalling an effective 60% outgo

For assets located outside India acquired from non-resident-period income or disclosed-but-undeclared foreign assets not exceeding ₹5 crore: a flat fee of ₹1 lakh

Payment Mechanism – Electronic verification; amount communicated within one month; payment due within two months; one-month extension with 1% per month interest

Immunity – Full immunity from further tax, penalty, and prosecution under the Black Money Act 2015 for income/assets declared and paid for up to 31 March 2026 or earlier years

Non-Applicability – Expressly excludes assets representing proceeds of crime under PMLA proceedings, and assets where Black Money Act assessment proceedings have been completed

Effect on Pending Proceedings – Assessing Officer required to take the declaration into account in finalising pending assessment orders

Board Powers – CBDT empowered to issue directions; Central Government empowered to make rules and remove difficulties within two years of commencement

The volume is divided into five self-contained Divisions, each prefaced by a detailed Arrangement of Sections or Arrangement of Paragraphs (for the Disclosure Scheme), enabling rapid section-level navigation. Within each Division:

The principal Act is presented first, in section-number order, with all amendments incorporated inline

Every amendment is footnoted with the amending instrument, date of effect, and prior text

Rules, regulations, and scheme texts follow the parent Act in logical order

Circulars and notifications are grouped at the end of each Division

Case law, where applicable, is integrated within the statutory text at the relevant section, annotated with citation references

The cross-referencing architecture across Divisions reflects the interconnected nature of the legislation—the Benami Act expressly cross-references PMLA’s definition of ‘proceeds of crime,’ while the Disclosure Scheme expressly carves out PMLA-proceeding assets and Black Money Act-assessed assets. The volume’s consolidated structure makes these cross-statute interactions immediately visible